Putting the facts at your fingertips

TAX TABLES

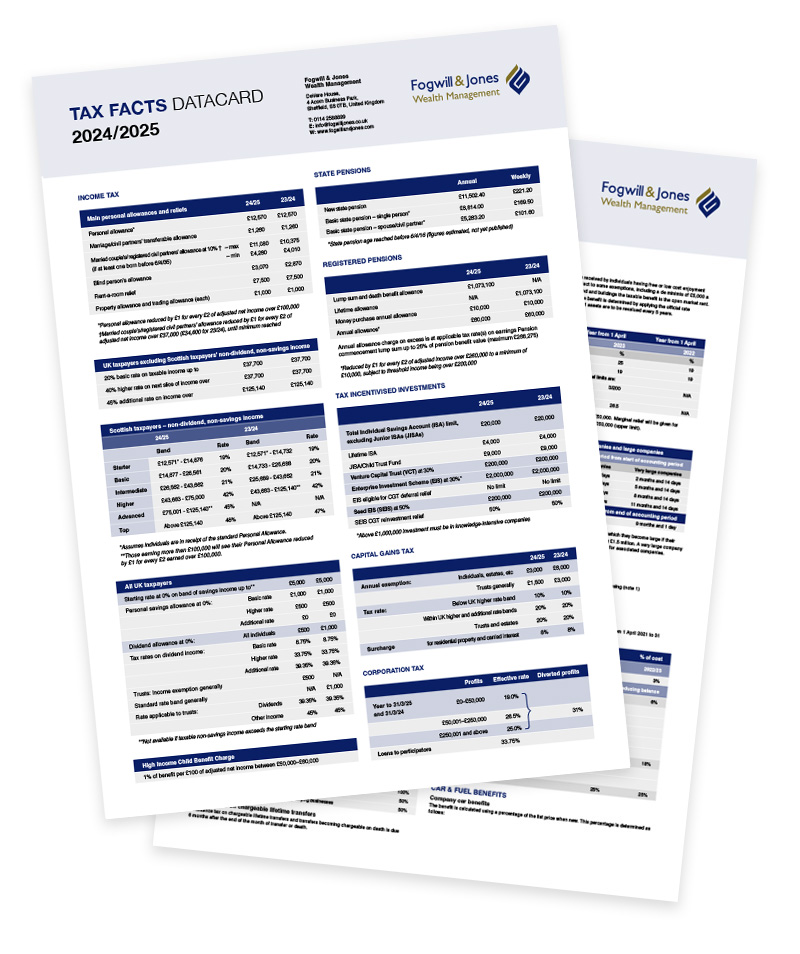

To Download a PDF version of our Tax Facts Datacard 2024/25, please click on the button below.

Privacy Policy | Terms & Conditions | Cookie Policy | Remuneration policy statement

Fogwill & Jones Wealth Management is a trading name of Fogwill & Jones Asset Management Ltd.

Fogwill & Jones Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. FCA number 433208. Registered in England and Wales. Registered office: DeVere House, 4 Acorn Business Park, Woodseats Close, Sheffield, S8 0TB. Company registration number 5459286. VAT Reg No 859 4216 95.

© Copyright 2023 Fogwill & Jones Asset Management Ltd. All Rights Reserved.

The Financial Conduct Authority does not regulate Will Writing, Taxation and Trust advice. Not all Inheritance Tax Planning solutions are regulated by the Financial Conduct Authority. The guidance and/or advice contained within this website is subject to the UK regulatory regime and is therefore targeted at clients based in the UK.